This is a paper on Marx’s notion of “capitalism” and Frank Knight’s notion of “civilization” and why both leave much to be desired.

Historical and Modern Arguments Against Contractual Slavery

February 8, 2026 by

This is a preprint of: Ellerman, David. 2025. “The Historical and Modern Arguments Against Contractual Slavery.” In The Palgrave Handbook of Modern Slavery, edited by Maria Krambia Kapardis, Colin Clark, Ajwang Warria, and Michel Dion. Palgrave Macmillan. https://doi.org/10.1007/978-3-031-58614-9_9.

Marginal Productivity Theory versus Labor Theory of Property

November 11, 2025 by

This paper shows that MP theory can also be formulated in a mathematically equivalent way using vectorial marginal products–which however conflicts with the “distributive shares” picture.

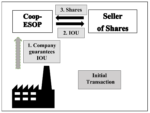

Market Valuations are Inappropriate for Employee-Owned Firms

October 11, 2025 by

Any `fair market valuation’ of an employee-owned firm or partnership that assumes those future residuals accrue to the current shareholder/residual-claimants is inappropriate.

Are Corporations the Problem?

May 26, 2025 by

Are corporations the problem? Can reforms in the area of corporate responsibility (e.g., more stakeholder governance) lead to any real changes? The goal of the paper is to analyse debates concerning the Citizens United case, corporate personhood, the stakeholder theory, the affected interests principle and, finally, deeper fallacies with respect to the rights of capital embedded in Marxism and conventional economic theories of capital and corporate finance.

Classical Liberalism and the Abolition of Certain Voluntary Contracts

May 19, 2025 by

This paper analyzes three contracts and shows that there is indeed a deeper democratic or Enlightenment classical liberal tradition of jurisprudence that rules out those contracts. The ‘problem’ is that the same principles imply the abolition of the employment contract, the contract for renting human beings, which is the foundation for the economic system that is often (but superficially) identified with classical liberalism itself. Frank Knight is taken throughout as the exemplary advocate of the economics of conventional classical liberalism.

Worker Cooperatives and Other “Cooperatives”

March 24, 2025 by

When is a “Coop” not really a cooperative? The short answer is whenever the actual activity of the “cooperative” is not carried out by the members but by employees. The problem is, of course, not in cooperation per se but in the hiring, employing, renting, or leasing of people to carry out the supposedly “cooperative” activities of the “cooperative.”

Fallacies about corporations

March 15, 2025 by

This article comments on Isabelle Ferreras’s “Democratizing the Corporation.” The focus is on the conceptual framing, which arguably contains a number of problems that are quite common on the left and are thus doubly deserving of commentary and explanation.

Opening the gates to Plato’s Heaven

March 15, 2025 by

The recipe to “open the gates to Plato’s Heaven” is by minimizing

the role of rivalrous substance and maximizing the role of non-rivalrous form. This creates a whole

series of different processes, positive feedback processes, vicious or virtuous circles, cumulative

circular causality, and increasing returns phenomena, which are analysed in this paper.