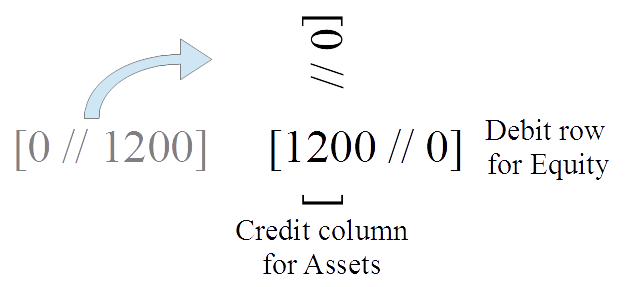

Double-entry bookkeeping (DEB) implicitly uses a specific mathematical construction, the group of differences using pairs of unsigned numbers (“T-accounts”). That construction was only formulated abstractly in mathematics in the 19th century—even though DEB had been used in the business world for over five centuries. Yet the connection between DEB and the group of differences (here called the “Pacioli group”) is still largely unknown both in mathematics and accounting. The precise mathematical treatment of DEB allows clarity on certain conceptual questions and it immediately yields the generalization of the double-entry method to multi-dimensional vectors typically representing the different types of property involved in an enterprise or household.

This publication represents success in a long struggle, stretching over three decades, to get the mathematical treatment of double-entry bookkeeping published in an accounting journal. Although the mathematical treatment and generalization of DEB was previously published in book form and in math and operations research journals, it seems to have been repeated blocked by the repeated refereeing of the author of the failed previous attempt at multi-dimensional DEB (see p. 493 in the paper).